Research Article | DOI: https://doi.org/10.31579/2578-8868/157

1* Associate Professor - Accounting Division - Faculty of Economics - University of Benghazi Financial Accounting, Benghazi, Libya,

*Corresponding Author: Moutaz A.Kablan, Associate Professor - Accounting Division - Faculty of Economics - University of Benghazi Financial Accounting, Benghazi, Libya,

Citation: Moutaz A.Kablan., (2021) The Impact of Chief Executive Officer Power on the Agency Costs: Evidence from Libya "An Applied Study on the Libyan Private Banks". J. Neuroscience and Neurological Surgery. 8(2); DOI:10.31579/2578-8868/157

Copyright: © 2021 Moutaz A.Kablan, This is an open-access article distributed under the terms of The Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited

Received: 02 January 2021 | Accepted: 01 March 2021 | Published: 12 March 2021

Keywords: agency costs; ceo power; agency theory.

Given that the importance of stabilization of the agency theory as a base to organize the relationship between the shareholders "the origin" and the management "the agent" in the business environment nowadays, this study aimed to identify the impact of the chief executive officer "CEO" power on the agency costs in the Libyan private banks. To achieve this goal the study underlying the scarcity of related previous studies has stated its hypotheses. The study sample consists of (6) private banks for (5) years; then the study relied upon the multiple regression technique, which has been used to examine the fourth sub-hypotheses of the main one. As a result, the study became able to state that there is a positive significant relationship between the CEO ownership in the bank shares and the agency costs, while that there is no significant relationship between the duality of CEO role, the duration of CEO in his position, the independency of the board of directors and the agency costs in the Libyan private banks.

At the outset, the agency theory idea presents the special relationship between the shareholders as the origin and the board of directors with all its relatives as the agent, who has the accreditation to invest their assets to maximize the firm value through time.

Although the propagation of this model as a basis to the complete independence between them through the spreading of shareholders companies except that there are some obstacles which have appeared as a case of the asymmetry information called agency costs [1].

Asymmetry information means that the agent has more deep information about the expected events and another sensitive insider information than the origin, so this flow will create a difficulty to monitor the agent performance fairly by the congress of owners [2]

Underlying this contradictoriness between this couple, the role of the chief executive officer "CEO" may affect negatively on agency costs, this is because that the CEO is the top of the executive management of the firm, so the agency theory believes that will never pursue toward maximization the returning of shareholders unless is available on appropriate corporate governance [3].

Speaking of the private banks in Libya, there are multi pure private banks have appeared in the Libyan economy consistent with the recent legislation which encourages this trend, but at the same time, these banks have suffered of multi crises during the last two decades, one of them is the agency costs problems.

And digression by mention of CEO exclusively of the authority of all managers compliance at the firm for all decisions by him. [4,5] indicate that there are four main sources that cause the CEO power like following:

Despite of, there are confirmations of the agency theory to the necessity of reducing the dominance of CEO about all conducts in the firm which targeted to avoid the negative impacts for this progressive power, but it must be acknowledged that there are multi benefits of that like idea response toward the emergency and expected cases [6].

From this point on, we can state that this controversial issue stills needs a lot of researches and studies, additionally; there are multi vital questions about the economic impacts of the progression of the CEOs power into their firms.

Accordingly, this study tries to answer the following question: what is the impact of the CEO power on agency costs at the Libyan private banks?

Literature Review and Hypotheses Development:

There are manystudies aimed to identify the factors those which affect negatively on agency costs. So, consistent with that and what have mentioned above about the question of study, the author will outline some of previous studies regarding to our study.

As what has mentioned before, the majority of the previous studies have stated that there are four main sources of CEO power: structural power, ownership power, expert power and prestige power, the study will present a summary of previous studies relying upon trend.

In the same direction, the study of [7] has determined the assets turn ratio to measure the agency cost as a dependent variable. The study outlined that there is non-significant relationship between the percentage of non-executive members in the board of directors and the agency costs. In addition, [8] have resulted that there is a positive relationship between the CEO ownership in the firm and the agency costs.

On other hand, [9]have presented different evidence about the relationship between the duration of CEO and the agency cost, due to the result ensured that there is a negative relationship between them.

Talking about the recent related studies, [10]has resulted in there is a negative relationship between the percentage of non-executive members in the board of directors and the agency costs, which measured by the assets turn ratio and the percentage of managerial expenses to the total of sales.

By digression, the study of [11]has stabilized to there is no significant relationship between the percentage of non-executive members of the board and the agency costs which measured by the two previous variables which were chosen by the last study.

From this point, due to the variance of the expectations about the impact of CEO power on the agency costs, the study became able to state the main hypothesis like the following:

H: There is no significant relationship between CEO power and the agency costs in the Libyan private banks.

Due to the CEO power sources as stated earlier, the study has derived the following four sub-hypotheses to examine the main one:

H1: There is no a significant relationship between the duality of CEO role and the agency costs in the Libyan private banks.

H2: There is no a significant relationship between the duration of CEO in his position and the agency costs in the Libyan private banks.

H3: There is no a significant relationship between the CEO ownership in the bank's shares and the agency costs in the Libyan private banks.

H4: There is no a significant relationship between the independency of the board of directors and the agency costs in the Libyan private banks.

The Importance of Study:

This study provides multi advantages to the investors due to getting acquainted with the impacts of growing the infiltration of CEO on the agency contract between the management and the shareholders which leading to make their investment decisions mature. Additionally, as far as the author knows this study considered as the first one in the Libyan business environment which tries to identify the impact of CEO power on agency costs.

This study mainly aims to identify the impact of CEO power on the agency costs at the Libyan private banks to present an applied evidence about the nature of this impact.

The methodology of study:

At first, the methodology presents all the steps during the trail either theoretical or applied aspects alike, so this section contents of the following sub-contents:

This study is based upon the inductive approach, whereas it has reviewed the related previous studies, the study has stated its main hypothesis and the four sub-hypotheses. Accordingly, the study has relied on deductive approach by statistical analysis to examine these hypotheses, to finally reach the findings and conclusion.

This section consists of the following sub-sections:

The population and Sample of Study:

The population of study consists of all the Libyan private banks, were they are shareholding companies basically. As for talking about the sample, it consists of the Libyan private banks which provide their published financial reports, additionally the external auditor report about the duration (2010-2014). These five years is the main condition to make the applied aspect complete relying upon the time series analysis.

Consequently, the purposive sample of study is shown in table (1) like following:

In addition, the study has stated the coming four models to test the four sub-hypotheses of the main one:

Agency Costs (it) = B0+ B1 CEO dual (it) + B2 board size (it) +B3 bank size (it) +B4 dividends (it) +B5 bgo (it) +B6 lev (it) + ∑ (it) ………..(1-1)

Agency Costs (it) = B0+ B1 CEO dura (it) + B2 board size (it) +B3 bank size (it) +B4 dividends (it) +B5 bgo (it) +B6 lev (it) + ∑ (it) ………..(1-2)

Agency Costs (it) = B0+ B1 CEO own (it) + B2 board size (it) +B3 bank size (it) +B4 dividends (it) +B5 bgo (it) +B6 lev (it) + ∑ (it) ………..(1-3)

Agency Costs (it) = B0+ B1 board ind (it) + B2 board size (it) +B3 bank size (it) +B4 dividends (it) +B5 bgo (it) +B6 lev (it) + ∑ (it) ………..(1-4)

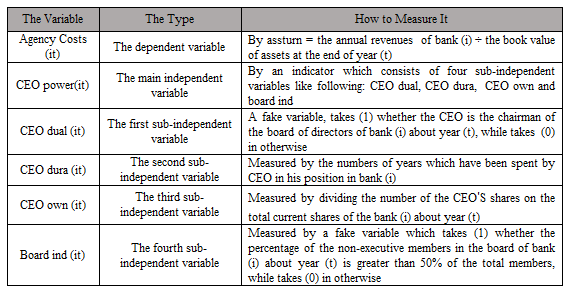

(5-2-5) The variables of study and How to measure them:

To achieve the statistical aspect of study, the author will rely upon assets turn ratio to measure the agency costs of the bank, so the following two (Tables 2,3) illustrate each variable and how to measure it:

An Important Note:

Take in your concern that the percentage of the assets turn ratio will be entered through the statistical analysis subtrahended of 100%, this is because the increasing of this percentage means decreasing in agency costs, and vice versa.

(5-2-6) The Results of Applied study:

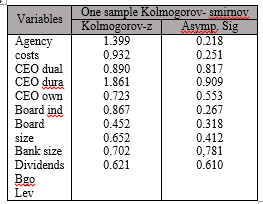

First and foremost, the author has relied upon Kolmogorov smirnov test to identify whether the collected data are normally distributed or not.

According to table (4) the results of test illustrate that the data are normally distributed "parametric", due to the Asymp. Sig "p-values" of all variables are greater than "α= 0.05".

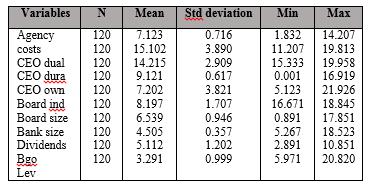

Table (5) shows the means, standard deviations, and the highest and lowest values of all study's variables.

H1: There is no a significant relationship between the duality of CEO role and the agency costs in the Libyan private banks.

According to the statistical analysis of model (1-1), the study has concluded that, there is no significant correlation relationship between the duality of CEO core and the agency costs in the Libyan private banks.

Where, calculated (p-value= 0.590) < (α= 0.05), so this sub-independent variable doesn't affect on the dependent variable "agency costs".

Consequently, the study rejected this sub-hypothesis (H1).

H2: There is no a significant relationship between the duration of CEO in his position and the agency costs in the Libyan private banks.

According to the statistical analysis of model (1-2), the study has concluded that, there is no significant correlation relationship between the duration of CEO in his position and the agency costs in the Libyan private banks.

Where, calculated (p-value= 0.510) < (α= 0.05), so this sub-independent variable doesn't affect on the dependent variable "agency costs".

Consequently, the study rejected this sub-hypothesis (H2).

H3: There is no a significant relationship between the CEO ownership in the bank's shares and the agency costs in the Libyan private banks.

According to the statistical analysis of model (1-3), the study has concluded that (adjusted R2 = 0.935), this means that %93.5 of the happened changes in agency costs in Libyan private banks can be explained by the CEO ownership in the bank's shares.

In addition, the results of statistical analysis confirm the significance of this effect, where that the calculated (p-value= 0.0001) > (α= 0.05), so this sub-independent variable significantly affects positively on the dependent variable "agency costs". So to test this model, the study has used "t" test, then the factor = 0.995 and t-value = 6.48.

This means that the CEO ownership in the bank's shares has a positive significant effect on agency costs.

Based on all of above, the study accepted this sub-hypothesis.

H4: There is no a significant relationship between the independency of the board of directors and the agency costs in the Libyan private banks.

According to the statistical analysis of model (1-4), the study has concluded that, there is no significant correlation relationship between the independency of the board of directors and the agency costs in the Libyan private banks.

Where, calculated (p-value= 0.530) < (α= 0.05), so this sub-independent variable doesn't affect on the dependent variable "agency costs".

Consequently, the study rejected this sub-hypothesis (H4).

The summarized Results:

It is possible to summarize the applied results like following:

Due to this study aimed to identify the impact of the chief executive officer power in the Libyan private banks as an independent variable, the author has derived this power to four sub-independent variables like following: the duality of CEO role, the duration of CEO in his position, the CEO ownership in bank's shares and the independency of the board of directors of the bank.

As a result, after the execution of the applied aspect, the study has resulted that there is no significant relationship between the first, the second, the fourth sub-independent variables and the agency cots in the Libyan private banks. While there is a positive significant relationship between the third sub-independent variable "the CEO ownership in the bank's shares" and the dependent variable of the study "the agency costs in the Libyan private banks".

Dear Editorial Team, Clinical Medical Reviews and Reports. My experience with the journal was highly positive. The peer-review process was rigorous, constructive, and completed in a timely manner. The reviewers provided valuable comments that helped improve the quality and clarity of our manuscript. The editorial office was professional, responsive, and supportive throughout all stages of the publication process. Communication was clear and efficient, and any questions were addressed promptly. Overall, I found the journal to maintain high scientific standards and an excellent publication workflow. I would be pleased to consider submitting future work to this journal. Best wishes from, Elena Popa.

It was my pleasure to submit my testimonial concerning the Reviewer Board of our Scientific Journal “Brain and Neurological Disorders”. The Reviewers focused on some modifications and their contribution was helpful. The ladies of our Editorial Office were also supported my efforts. It was my honor to have such a co-operation and I am looking forward for more collaboration.

Dear Grace Pierce, Editorial Coordinator of Journal of Clinical Research and Reports, Thank you for the speedy and efficient peer review process. I appreciate the fact that your peer reviewers do not take months to respond like with some other journals. I would also like to thank the editorial office for responding quickly to my questions. It is an excellent journal. I plan to submit more manuscripts in the future. Best wishes from, Robert W. McGee

Dear Grace Pierce, Editorial Coordinator of Journal of Clinical Research and Reports, Working with you and your team on our recent publication in JCRR has been a truly wonderful and enjoyable experience. The responses were prompt, and the reviewers were patient, constructive, and highly professional. One reviewer in particular gave me the feeling that a professor was carefully reading and commenting on my coursework, which was deeply touching. The entire process was straightforward and hassle‑free, with no tedious online forms to complete. I highly recommend this journal. Best wishes from, DR Aibing Rao, Head of R&D

I Appreciate the Opportunity to Share my Experience with the Journal of Clinical Research and Reports. The peer review process was timely and constructive, and the feedback provided helped improve the quality of our manuscript. The editorial office was professional, responsive, and supportive throughout the process, ensuring smooth communication and efficient handling of the submission. Overall, it was a positive experience collaborating with your team.

Dear Mercy Grace, Editorial Coordinator of Obstetrics Gynecology and Reproductive Sciences, We would like to express our gratitude for your help at all stages of publishing and editing the article. The editors of the magazine answer all the necessary questions and help at every stage. We will definitely continue to cooperate and publish other works in the Obstetrics Gynecology and Reproductive Sciences! Best wishes from, Alla Konstantinovna Politova,